Only about half of Americans are familiar with 529 savings plans, and only about 35% of parents are actually using them.

This is unfortunate, as a 529 savings plan is a great tool to have in your college planning toolbox.

As with any financial product, 529 savings plans have advantages and disadvantages, so it is imperative that parents evaluate their options before diving headfirst into the ocean of college savings alternatives.

Understanding the Basics: What Are Section 529 Plans?

Most of us are keenly aware of 401(k) plans. Just as 401(k) is a section of the IRS Tax Code, Section 529 is the section of the code that deals specifically with college savings plans.

There are two basic types of plans: prepaid tuition plans and savings plans. Generally, when people talk about 529 plans, they are referring to the savings variety. We will follow this convention and focus solely on the 529 savings plan below.

If you want to explore prepaid tuition plans, please check out this blog post.

A 529 savings plan is an investment account that grows tax-free and can be withdrawn tax-free IF used to pay for qualified educational expenses for a beneficiary. In addition to traditional college expenses (e.g., tuition, room & board, books, computers), you can also use your 529 to pay for the following without penalty: K-12 tuition, apprenticeship/trade programs, and up to $10,000 in student loan repayments.

Each state sponsors at least one Section 529 savings plan, and many states have multiple options.

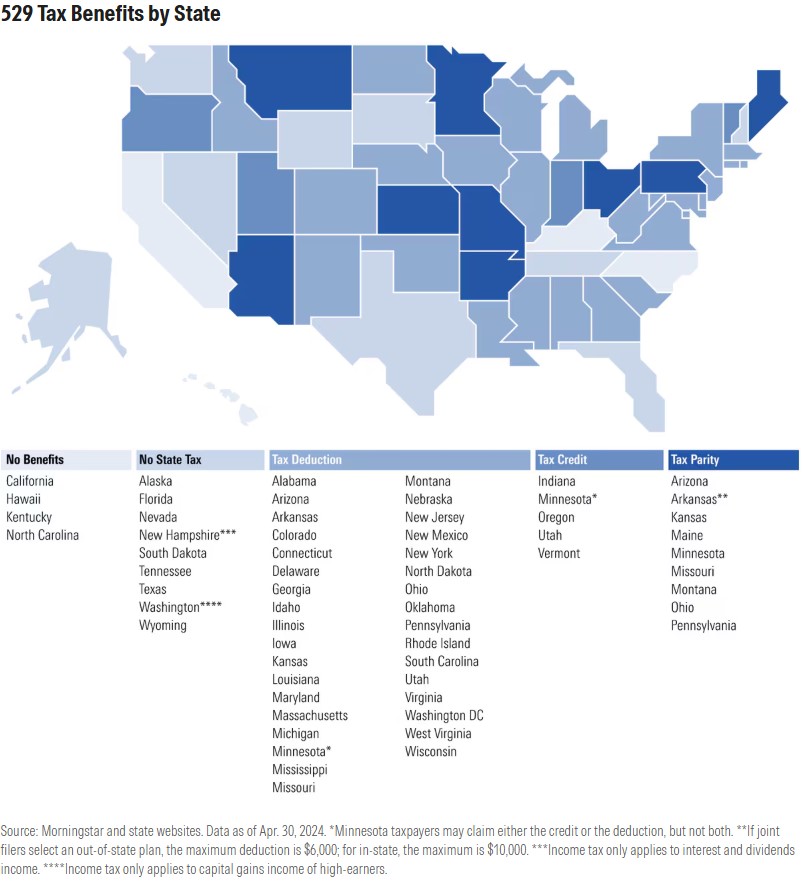

Tax Benefits of 529 Savings Plans

Federally, and in many states, the growth of the portfolio is tax-deferred, and distributions are tax-free as long as they are used for qualified higher-education expenses, including tuition, room and board, fees, books, computers, supplies, and more.

For a full list of 529 qualified expenses, click here.

In addition, a majority of states allow tax deductions or tax credits for contributions to 529 plans. Some states offer tax deductions for only those living there, some offer deductions to anyone, and some don’t offer any at all.

As an example, Virginia offers state residents a $4,000 tax deduction per beneficiary, per plan, per year. If a contributor puts in $4,000 in a given year, they may carry forward those deductions to tax returns in a subsequent year.

Some states, such as Indiana, offer state residents a 20% tax credit of up to $1,000.

Simply put, the tax-deferred growth and tax-free distributions make this a savings plan worth considering.

To figure out what plan is right for you, check out our 529 State Tax & Fee Calculator:

![]()

529 Savings Plans Versus Traditional Brokerage Accounts

Brokerage accounts are supremely flexible in that you can take money out at any time and use it for whatever you desire. The primary issue with traditional brokerage accounts is taxation on multiple fronts.

On the other hand, 529 plans are specifically designed to save for education. They are targeted toward college savings and encourage early and consistent contributions by offering a tax-advantaged and convenient way for families to save for their children’s college education.

While they may not have the flexibility of a traditional brokerage account, 529 savings plans do not necessarily “lock you in.” If you overfund your 529 or one of your children decides not to go to college, you can easily switch the beneficiary to another family member. You can also now transfer up to $35,000 of unused funds to a Roth IRA.

The main issue with these plans is as follows: if you use the money for non-qualified expenses, you must pay income tax on the earnings and a 10% penalty.

Ultimately, paying for college is not about choosing one vehicle over another; it’s about finding the right combination of tactics appropriate for your unique family situation and goals. Some families may already have brokerage accounts for mid-term and long-term savings, which can be used to bolster college savings.

Some families might also consider adding another tax-advantaged account, like a Roth IRA, to their college funding plan. The Roth can be used for education expenses without penalty and is not counted as an asset on the FAFSA.

529 Plans and Financial Aid

Some families worry that the money in their 529 accounts will hurt their financial aid eligibility. In reality, 529 savings plans only reduce your financial aid eligibility by a maximum of 5.64% of the asset’s value. Contrast that with a student-owned asset, such as a UTMA or UGMA, which counts against you at 20%.

Furthermore, with a 529, the parent retains control of the funds, which tends to be a prudent strategy. Surprisingly, 18-year-olds often struggle with managing inherited wealth.

Other benefits of 529 savings plans:

- Most plans have very low minimum monthly contribution limits.

- The beneficiary can be changed at any time to another member of the beneficiary’s family.

- Money can be used at virtually any accredited college in the country.

- Account owners can make a lump-sum contribution of up to $95,000 per beneficiary or $190,000 if married filing jointly and avoid incurring a taxable gift on this amount by electing to use five years of the annual gift tax exclusion all in one year. Learn more here.

529 Savings Plan Disadvantages

Market Volatility: Although most financial and college experts champion 529 savings plans, it is essential to remember that these plans are tied to the stock market, which inherently carries risk. You will see peaks and troughs—and potentially, massive troughs at inopportune times. Ensure your plan has an age-based allocation that becomes more conservative as your child approaches college age.

What happens if a family’s prized college funding asset—the 529 plan—suddenly becomes a “229 plan” in the year before your child heads off to school? You want options and contingencies in place to keep you afloat when something like this happens. This is where a financial planner who knows the college funding game can help you.

Limited Investment Options Compared to Brokerage Accounts: This does vary by state and plan. Some are much better than others. You can research that here.

Flexibility: 529 savings plans can not be used with the same flexibility as a brokerage account or Roth IRA. You must use the money for qualified expenses, or you will have to pay income taxes on the earnings plus an additional 10% penalty.

The Bottom Line: Is a 529 Savings Plan Right for You?

So, do the pros outweigh the cons? As with any investment, it is imperative that you evaluate all of your options.

Often, a combination of tools is the most effective approach.

The value of higher education is still cherished in today’s society, yet paying for it has become more and more difficult.

With dollars already stretched thin in today’s economy, it is important that your family create a comprehensive financial plan for college with contingencies for all of the curveballs that will come your way.

I think we can all agree on one thing—the cost of a four-year college education will not be getting dramatically less expensive any time soon.

Determining whether a 529 savings plan is right for your family is an important decision; what is more important is that you do something. If you’ve got young children, the good news is that you’ve got time on your side. The bad news? Well, the bad news is that you’ve got time on your side.

Talk to a college funding expert here:

Author:

Related Reading: