Many parents already have enough on their plate as they try to secure their retirement. Throw college into the mix and things get much more complicated.

Nevertheless, the majority of parents still plan to fund part of their children’s college—about 70% of them according to a Fidelity study in 2018.

What’s worrisome is that some parents may be inclined to dip heavily into their retirement funds to help their kids out. Most financial planning experts warn against this. There is a myriad of ways to deal with college expenses—retirement, not so much.

What’s more worrisome is that some parents believe it’s an either/or situation: you either sacrifice retirement funds or you sacrifice your kids’ college. Not true. There are strategies to handle both.

The Retirement Accumulation Cycle

It is crucial to start your accumulation cycle for retirement as soon as possible. The earlier you start saving, the more time you have for those contributions to compound. We really only have one major compound growth curve throughout our lives. Starting this growth cycle all over again reduces all the work your money was doing for you. And you can’t turn back time.

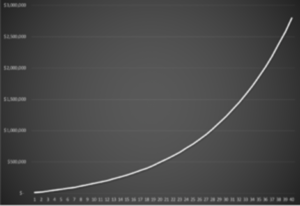

Here’s a basic chart of a 40-year accumulation cycle:

Notice how much growth occurs on the backend!

A massive expense like college would deplete these cash accounts and restart your growth cycle. In doing so, you would curb your ability to reap the rewards on the backend and run more risk with historic ups and downs. You are not just taking a step back; you are leaping back. What happens then? You desperately have to play catchup!

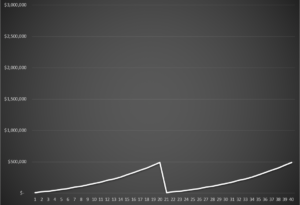

Here’s the same chart but playing out the scenario where you pull out retirement funds for a big expense:

How Do We Save and Spend Money Efficiently Then?

Accumulation using several different financial vehicles is a must.

Unfortunately, many financial strategies focus only on the accumulation of money and not the distribution. The ability to access cash from your retirement accounts with convenience and efficiency, while minimizing risk, expenses, and taxes is of critical importance.

College is typically the “last biggest” expense before retirement. The average age of parents with children in college is typically early to late ’50s. There’s not a lot of room for financial mistakes at this point in life if you intend to retire comfortably.

Definitely Don’t Use Your 401k to Pay for College

In case you are still not convinced, here are the main drawbacks of tapping into your 401k:

- There may be a 10% tax penalty on early withdrawals below age 59½.

- A potentially bigger tax bill the year of withdrawal as the money you withdraw is counted as income.

- Loss of tax-free growth of your savings.

- Income will also be counted in financial aid calculation.

Let this sink in: if you take out a loan on your 401k, you hinder your pre-tax accumulation, AND you have to pay the loan back with after-tax dollars. When you start withdrawing for retirement, you will have to pay taxes on the after-tax dollars. Yep, your money gets taxed twice! This completely negates the benefits of the 401k.

On the other hand, putting money away in retirement accounts (and keeping it there) actually helps you when it comes to need-based aid! The FAFSA does not assess money in IRAs/401K’s.

The Importance of Timing Distributions and Increasing Cash Flow

An experienced professional will tell you that timing the market for long-term growth is not a good strategy, but time IN the market is crucial.

Timing the market DOES matter, however, when it comes to distributions. As we all know, the rule of investing is to buy low and sell high.

In this scenario, we’re not talking trading stocks, but rather the “buying” is taking the distribution and the “selling” is not touching that account and letting it rebound while you utilize other accounts. For example, if we’re in a market where investment accounts like Section 529 Plans are down, it may not be a smart strategy to take a distribution from that asset class.

Of course, this all depends on your unique family and financial situation. Maybe it makes sense to utilize that cash-value life insurance that has not taken a hit. Maybe you have a high school senior, and he/she takes a gap year and works while you give yourself time to increase cash flow and let your investment accounts bounce back. Maybe, you have a junior in high school as well—if those two kids go to college at the same time, you may qualify for more aid!

The point is, there are strategies out there that are far better for you than touching your 401k.

Volatility Buffers: Protecting Against the Unknown

With the arrival of COVID-19 and the resulting repercussions, we received yet another reminder to have some money that is shielded from the market.

The unknown makes planning challenging. There is no one-size-fits-all financial plan. But there are steps everybody should take to ensure they are protected against the unpredictable.

One of these steps is to mitigate risk and retain flexibility through diversification. Yes, most people know this, but it is imperative to have money in different “buckets,” and these buckets should not all be hanging on the same rope. Having a bucket that’s not connected to the market can be a gamechanger in difficult times.

Utilize Flexible Assets

Here are a few financial vehicles that you could use to save for college and/or retirement efficiently. Remember, these are helpful tools; they are not comprehensive strategies!

Section 529 Plan – The 529 has become very popular as a tax-advantaged vehicle specifically designed to save and pay for college. The major drawback is that the account can only be used for qualified education expenses (without taking the penalty), but even if none of your children go to college, you can use it for yourself or your grandchildren.

Roth IRA – Although technically a retirement account, there are many aspects of the Roth that make it useful for college as well. Here’s a post on how and why you might use a Roth IRA for college.

Cash Value Life Insurance – This one is all about the long-term. Many people are hesitant to utilize this asset because of possible hidden fees and policy fine print. Truth is, if you work with a dependable financial professional and you understand what you are buying, you can have a bucket of money that is not tied to the market and does not count against you in the financial aid calculation.

It is important to stress that these are tools to be used within a comprehensive financial plan that maximizes the efficiency of your money. They are not silver bullets!

Final Thoughts

- You can’t just come up with the money for retirement when it hits – you need to use time to your advantage and work that back-end accumulation.

- Saving for retirement is the priority, but that doesn’t mean you can’t prepare for college at the same time.

- Meet with a college funding expert early on to come up with a financial plan that will help you use your money efficiently and enable your child to get more financial aid.

- Saving and spending your money efficiently is important but there are other options out there for your child if you can’t pay for them: financial aid, scholarships, student loans, community college, etc.

A Note on Financial Planning

Most people view financial planning as a fairly simple, linear process. It’s a little more complex than that. Life, money, and the economy do not necessarily work in a linear fashion. Too many factors affect our financials, such as unexpected life twists and turns, inflation, fees, sequence of return risks, taxes, timing, etc. that it’s best to have a financial plan that delves into college and retirement.

Although it may not be a simple process, you should not have to sacrifice college for retirement. And you should never sacrifice retirement for your kids’ college. It’s important to create a financial plan early so you can get on top of this. Even if your kids are older, it’s not too late to employ these financial strategies.

And sure, you can handle it on your own; many people do. But our coaches at the College Funding Coach are here for you if you don’t have the time, expertise, or interest to plan for college and retirement!

For many families, the high cost of higher education is a daunting proposition. The College Funding Coach is here to help. To learn more about paying for college while saving for retirement, register for one of our free workshops/webinars or speak with a coach to get started on your college funding journey.

Author: