Beginning in 2024, leftover money in a 529 College Savings Plan can be redirected to a Roth IRA without penalty for a qualified beneficiary of any income level.

For this new update, we can thank 2022’s Secure Act 2.0.

Why This Might Benefit You

Why is this update an interesting and noteworthy benefit for owners and beneficiaries of 529 plans?

In the past, families who had leftover education funds in a 529 account (with no immediate family members to whom the funds could be transferred) had two primary choices:

- Leave the funds in the account to kick-start college funding for potential grandchildren.

- Distribute funds from the account for non-qualified expenses.

While, if necessary and suitable, either option has its arguable benefits, they both have considerable drawbacks.

While saving money for future grandchildren is admirable, some parents have more urgent financial needs or goals. Plus, grandchildren are not guaranteed.

For the second option, withdrawing money from a 529 plan for non-qualified expenses results in both a 10% tax penalty and a tax payment on the previously non-taxed gains from the account.

Now, we have a third option to consider for those lucky enough to have the challenge of deciding what to do with excess 529 funds. Let’s explore it…

529 Transfer to Roth Requirements

1. A qualified beneficiary is overwhelmingly going to be the original beneficiary, not the owner, of the eligible 529 plan.

2. The 529 plan must have been open for at least 15 years to be eligible for funds to be transferred to a Roth IRA in the name of its qualified beneficiary.

3. The funds to be moved into the Roth IRA cannot have been contributed to the 529 account within 5 years of transfer to a Roth IRA.

The good news: parents who own overfunded 529 plans for their children can now give them the gift of both education and a tax-free retirement savings account, albeit a slightly limited one.

Parents who opened 529 accounts more recently can wait out the 15 years and know that the money growing tax-free inside of the 529 account can be transferred to their child(ren) tax-free and penalty-free in just a matter of time.

There has been some speculation that the account owner can change the beneficiary to himself or herself, which resets the 15-year clock at the time of change. Time and experience will reveal whether this speculation turns out to be true. Depending on the IRS’s interpretation, this law could become a wealth transfer and tax strategy for estate planning.

529 to Roth Limitations

Transfer Cap

As much as we’d like it to be, there is not an unlimited opportunity to move excess educational funds to retirement. The maximum allowable transfer from a 529 to a Roth IRA is $35,000, and the transfer must follow the Roth IRA contribution rules.

In 2024, the Roth IRA contribution limit is $7,000 for those under 50 and $8,000 for those 50 and older.

The first $7,000/$8,000 of the $35,000 transfer can be made this year for eligible qualified beneficiaries, and then you would continue to follow the max contributions until you hit $35,000.

There have been whispers that this is a disadvantage because the new graduate is not able to personally max fund a Roth IRA if the funding is coming from the 529. However, I know a young 20-something or two who would be thrilled to have extra funds to re-direct for a few years while being the grateful recipient of Roth IRA funding from leftover college funds.

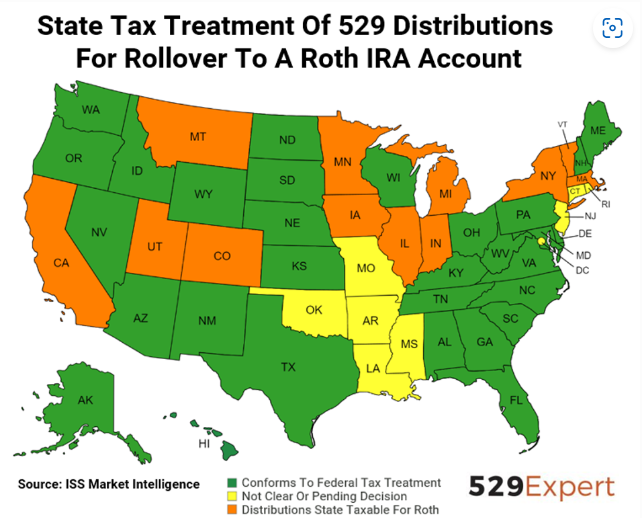

State Tax Quirks and “Clawbacks”

You know how some states give you a nice tax deduction for contributing to a 529 Plan? Well, some of them might want it back when you transfer funds to a Roth.

Depending on the state, the transfer may be viewed as a nonqualified rollover. As a result, the rollover may be subject to state income tax on the earnings and/or tax benefit “clawbacks.” Take a look at the chart below, courtesy of Forbes, which shows how each state treats the 529 to Roth Rollover (as of March 2024):

Prepaid Tuition Plans

When we talk about 529 Plans, we generally discuss the more popular savings variety. However, there are still some states where prepaid plans are quite popular.

Each prepaid 529 plan has a different set of requirements and restrictions when it comes to the Roth transfer.

If you own a prepaid tuition plan, make sure to check with your plan administrator to see what your specific process entails.

Final Thoughts…And More Questions

Most experts are preaching caution to those considering moving their 529 funds. Why? We are still waiting on more clarification from the federal government due to the underlying statutes being rather vague. No one seems to know how exactly this process works yet.

For example, there are tons of questions regarding the 15-year clock and how it’s affected if you change the beneficiary.

So, stay tuned. We will keep this article updated as more information comes out.

In this prevalent cultural conversation about the high cost of education, this change will hopefully inspire more confidence in your decision to use the 529 savings plan as a strategic tool to help pay for your kids’ college and, if the stars align, a little piece of their retirement.

If you’d like to to learn more about a specific college funding strategy and if this new law can benefit your family, one of our college funding coaches will be happy to talk to you:

This article is solely intended for educational purposes. For recommendations or advice regarding your unique financial situation, please talk to your financial advisor.

Author: