Post updated October 21, 2024. We hosted a free, live webinar on this topic on October 18th, 2024.

College is not paid at sticker price!

Yes, you read that correctly. If ten students went to the same college at the same time, all ten might pay a different price for the same college. Now, how is that even possible?

Welcome to the absurd world of paying for college! It’s like going shopping with sales and coupons; everyone can buy the same item at a different price (except no one understands all the costs involved from the outset). Or, maybe you’ve heard of the airline ticket analogy, where hundreds of people get similar seats for different prices.

Given the murky nature of the college pricing industry, learning the rules of financial aid is a MUST. Knowledge of this system can save you thousands of dollars.

Let’s take a look at some of the rules…

1. Fill Out and Submit the Financial Aid Forms: FAFSA & CSS Profile

I can’t stress this enough. I hear so many people say they didn’t get anything from the college, and I ask, “Did you fill out the FAFSA?” The answer is usually one of two things:

A. We make too much money, so what’s the point of filling it out?

B. What’s FAFSA? (often pronounced wrongly as “FASFA”)

Well, here’s your answer! You can’t win the lottery if you never buy the ticket.

Okay, it’s not exactly like the lottery–there is methodology involved–but the point is, you need to toss your hat into the ring.

Even if you think that you will never qualify for any aid, you should still submit the FAFSA. Why?

Submitting the FAFSA will open opportunities you may not have previously been aware of. Yes, you may qualify for federal subsidized loans or work-study — but did you know that many colleges require you to submit the FAFSA so they can determine what sort of merit aid package you are eligible for?

At the very least, it is helpful for colleges to have your info on hand in case something happens that negatively impacts your finances.

Additionally, everyone who submits the FAFSA can access unsubsidized federal loans, which are not based on need and can be a helpful part of your financial plan.

The FAFSA typically opens on October 1st of the student’s senior year in high school; it is generally a good idea to submit it as soon as you can. This year, the FAFSA will open in December (exact date TBA).

Parent Tip: Several parents in our private Facebook group suggest waiting a few days to submit once the FAFSA portal opens. The website tends to glitch or crash a lot in the beginning.

Remember, submitting the FAFSA is not a one-time thing. You must apply every year for which you are trying to receive financial aid.

The CSS Profile

Some colleges require you to fill out an additional form to access aid–the CSS Profile. This form is often required by private colleges and public universities with large endowments. They want to dig further into your financial situation to ascertain where to disburse their funds as accurately as possible.

The CSS Profile costs $25 for the first submission and $16 for every school after that. It is possible to get these fees waived.

The CSS Profile goes much more in-depth than the FAFSA. You will likely answer questions about your retirement accounts and primary home equity. Conversely, colleges that use the CSS Profile often have more flexibility and consider things like unusually high medical debt.

Beginning this year, the FAFSA will now assess family farms and businesses (even those with less than 100 employees)

The other significant difference between the FAFSA and CSS Profile involves divorced parents. Most CSS profile schools request that the noncustodial parent fill out the form.

Here’s the list of schools that require the CSS Profile and whether they require the noncustodial parent to submit their financial information.

To learn more about the CSS Profile, check out this post: A Guide to the CSS Profile.

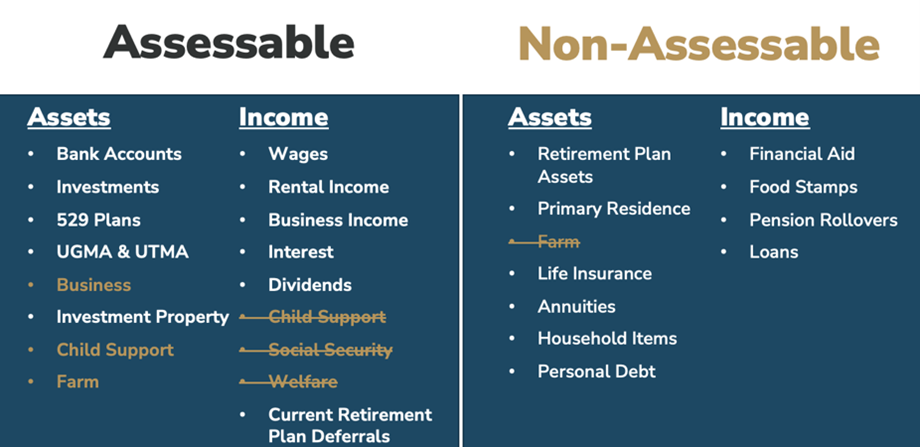

2. Know What’s Counted and What’s Not on the FAFSA

Some assets and liabilities are considered assessable for the FAFSA (meaning they count against you in the financial aid calculation), and a few are not counted.

For example, equity in your primary home is not counted, while investment property is. Non-qualified money in the bank and brokerage accounts is counted, while retirement assets are not.

Life insurance and annuities are not counted on the FAFSA. The Picasso on your wall and the Ferrari in your garage are not counted (personal effects), but your business is counted no matter what.

Knowing the rules and planning ahead of time helps tremendously if you want to maximize financial aid.

Here’s a more detailed rundown of what’s counted and what’s not:

Notes: Gold bullet points indicate FAFSA changes implemented for the 2024-2025 award year.

- Child support used to count as income but is now counted as an asset.

- Social Security and welfare programs are no longer counted.

- Business/Farm (except for the personal home on the farm) is now counted as an asset.

3. Who Owns the Asset & How Is Income Assessed?

The owner of the asset is very significant in the financial aid formula.

For the FAFSA, a parent’s asset is counted at a smaller percentage than the student’s. Parental assets are assessed at up to 5.64% of the asset’s value, while student assets are assessed at up to 20%.

As a general rule, any assets should be in the parent’s name instead of the student’s. For example, a UTMA, seen as the child’s asset, would be counted much more heavily than a 529 Plan (seen as a parent asset).

Ultimately, however, the FAFSA calculation is primarily driven by income. Parent income is assessed on a scale from 22% to 47%. While the new formula increased the parent income protection allowance, the sizeable discount for having multiple kids in college was removed.

The student’s income is counted at a flat rate of 50%, but fortunately, the student income protection allowance for dependent students is fairly high, sitting at $11,510 for the 2025-2026 award year.

The FAFSA looks at your income from the prior-prior year, so if your student starts college in 2025, you will provide your 2023 income info.

4. Grandparent Contribution

Grandparent cash support and distributions from 529 plans will no longer be counted as student untaxed income. This is HUGE!

Historically, families who might have qualified for financial aid have been penalized for this because distributions from a grandparent-owned 529 plan were counted as untaxed income for the student.

There were two ways around this. One was to transfer account ownership to the parents to avoid the distributions being counted as untaxed income for the student.

The second solution was to wait until the second semester of sophomore year to take distributions from the grandparent 529 plan. Remember, the FAFSA looks at prior-prior year income.

However, considering the cash support and untaxed income changes on the FAFSA for next year, all of the maneuvering mentioned above should be unnecessary.

We realize this may all be very confusing, so if you’d like to speak to an expert on how to maximize aid or cash flow, please reach out for a free consultation with one of our college financial planners:

5. Multiple Kids in College Simultaneously

Previously, if two or more children were attending college simultaneously, a family’s EFC would be divided among the number of students. This rule is now obsolete.

There is still some good news:

- Financial aid administrators have the discretion to consider the multiple-kid situation.

- Most CSS Profile schools appear to be keeping the old rule in place. This may cause even more CSS Profile schools to become as affordable or more affordable than FAFSA-only schools.

6. Private College vs. Public College

Many parents believe their child can go to any college as long as it is public in-state. While not a terrible approach to take, it is very limiting.

Many private colleges have large endowments relative to their student population and more flexibility with their money, meaning they will open up their wallet if they want to attract your student to the school. With more money to spread to fewer students, private schools tend to have a higher capacity to give need-based aid AND merit aid than public colleges.

So, if nothing else, don’t rule out private colleges. Furthermore, even some out-of-state public schools may even be affordable.

7. Divorced Parent Change

The new FAFSA rule states that irrespective of which parent the kids live with, the parent who provides the greater financial support to the child in the prior-prior year is counted as the custodial parent. If this is equal, the parent with the higher AGI is counted as the custodial parent.

Previously, it was based on where the student lived 51% of the time.

8. “Negotiate” with Colleges

I put the word negotiate in quotes here because the stewards of higher education do not want the perception that this is a business transaction. So, don’t use the word negotiate.

Nevertheless, you can discuss cost and aid with college financial aid and admissions officers. If your child is admitted to a school, it is in the school’s best interest to get you to attend.

I have seen colleges go all out to better their financial aid offers when shown an aid offer from a rival college.

But the catch is this: you have to take an active role in politely reaching out to the financial aid & admissions offices, talking to them, and then going back and forth with several colleges till you get an offer you can’t resist. You must be ready to walk away from a specific college for this to work. This can be a massive emotional challenge to your child, so it’s a good idea to sit down and have the money/college talk with your kids as early as possible.

9. Professional Judgement Letter – Official Financial Aid Appeal

If your financial circumstances have changed after you filed the FAFSA, then you can submit a request for Professional Judgement to the college, explain your situation, and see if they will reconsider your financial aid package.

Things that constitute a change would be if your parent lost their job, died, or became disabled. The financial aid office would have the final say in this, but it does not hurt to reach out. This is a formal process, but each college may have its own instructions for how you submit your info.

One common reason for a family to appeal is that their income from the prior-prior year is not an accurate depiction of the family’s current financial situation.

There are two major updates to Professional Judgment that you should know:

- Unusual business, real estate, or investment losses can now be considered as special circumstances.

- If a parent can show evidence of application for or reception of unemployment benefits in the last 90 days, a school can set the parent’s income to $0.

10. Loans

Lastly, I would say that if you still have a sizeable college funding gap and you have to take student loans for college, be wary of the Parent Plus Loan option that comes bundled in many college financial offers. It has a higher interest rate and higher fees than direct federal loans and sometimes even loans on the private market. The added danger of Parent Plus Loans is that you can access funds up to the cost of attendance for college with relative ease.

While private loans should be your last resort, there are many loan options out there from private lenders that come at a lower interest rate than the Parent Plus Loans if the parents have good credit. Check out Sallie Mae, Commonbond, or Simple Tuition.

Before choosing the private student loan route, though, run through this list: 14 Ways to Minimize Student Loans.

Families get stuck in student debt trouble because they don’t adequately plan for college or find the right financial fit and say they “will make it work.”

Those who know the rules and strategies as early as possible gain a distinct advantage in the college funding game.

So, plan, plan, and plan some more!

Author:

Zaina Bankwalla, MBA, CFBS, RICP, CEPA