The Financial Dilemma: College or Retirement?

A 2022 Fidelity Study found that saving for college is the number one financial priority for most parents. Another study, this one from Lending Tree, discovered that 68% of parents consider withdrawing retirement funds to help fund college.

The dream of a college education for your children is a noble one, and as parents, it’s only natural to want the best for your kids. However, the rising cost of education, coupled with the fact that most parents are in their 40s and 50s when their children go off to college, creates a significant financial challenge.

Below, we’ll explore the intricacies and consequences of this financial dilemma, as well as possible solutions.

Age Factor

As noted above, by the time kids are ready to go to college, their parents are at an age where retirement is starting to loom large. This generates more urgency and earnestness in building and preserving a nest egg. This is a prime age for career progression and earning potential; it’s also the time when retirement planning should be in full swing.

College throws a massive wrench into this equation.

When parents divert a significant portion of their income to pay for their children’s education, they may inadvertently miss out on years of potential compounding.

Lost Opportunity Cost – Cutting Into Compound Growth

The primary factor in this college vs. retirement dilemma is lost opportunity cost. Every dollar that you spend on college is a dollar that you will never have for your own retirement, a dollar that could’ve earned interest.

Wealth building is a function of savings, time, and rate of return. The more time we save and utilize compounding, the more wealth we will build. In a 40-year saving cycle, the most significant jump in growth always comes in the last few years before retirement.

It’s crucial that you have the largest pile of money already saved in the last few years before you retire so you can harvest the miracle of compounding growth.

Many parents attempt to restart or ramp up their retirement savings after the “paying for college years” but often find themselves in a hole because of the lost opportunity cost.

Ergo, college funding is inherently a retirement problem and should be incorporated into any holistic financial plan.

And the number one rule of college planning? Never sacrifice your own financial security for your children’s education. It sounds callous and cold, but this usually benefits both sides in the long run.

The Miracle of Compound Interest

Most of us understand the miracle of compound interest. You may not understand the math or technicalities, but you surely understand the result.

Interest, however, is just one factor in the compounding story. The second is time, and that is of the essence.

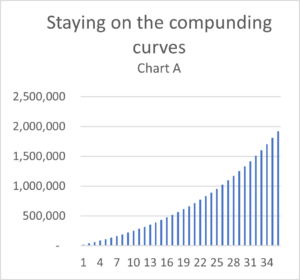

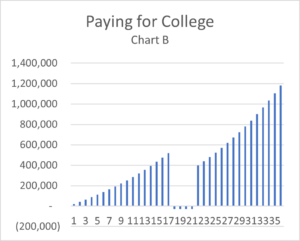

Let’s look at a hypothetical example; let’s say you were saving $20,000 per year in an account where your money could grow at a hypothetical 5% annually.

At the end of your working life of 35 years, you would have a little over $1.9 million (Chart A). But what if, along the way, you paused your retirement growth cycle, paid for college for four years, and then restarted again after graduation (Chart B)? At the end of the same 35 years, you would have a little under $1.2 million. A difference of about $700,000. This is money lost because you got off the compounding curves for four years; this is money you can never recoup.

Hopefully, you’ve realized that retirement takes priority. There are myriad ways to fund college or even take an alternative path; this is not the case for retirement.

Avoid Restarting the Growth Cycle

Traditional financial planning is all about mutually exclusive buckets. Let’s save money for retirement in this bucket called a “401(K) or IRA” and let’s save for education/college in this other bucket called the “529 plan.” Both these buckets are to be used for their respective purposes. In general, if you start saving early and often, this may work well enough.

But more often than not, reality thrusts its imperfections into the works.

What happens if you’re not meeting your retirement goals? What happens if you have major unforeseen expenses? What happens if your child gets a large scholarship or does not go to a traditional college at all?

Should you use this leftover money to fund your retirement?

The answer is usually no.

You cannot and should not use it for your retirement unless you are willing to pay taxes and penalties. Now, maybe these taxes and penalties are negligible to you in the long run, but often it makes sense to preserve your tax advantages.

For example, you can always transfer a 529 plan to the next child or save it for grad school. Additionally, starting in 2024, you can roll over some 529 money into your child’s Roth IRA.

Do you see the problem, though? Once you allocate money toward college in a college-funding bucket, it appears to be gone forever. There is no way to recoup what you spend on college.

The Student Loan Problem

The most common advice given by financial planners regarding college vs retirement is this: your student always has the option to take out loans for college, but nobody’s going to offer you a loan to retire.

Many parents will not be able to cover their childrens’ college expenses outright, but they still want to support their kids’ education. In such cases, student loans often come into play. The key here is to stick to federal direct loans if possible.

Taking on significant student loan debt via parent PLUS or private loans (when the parent co-signs) can be even more detrimental to parents’ retirement plans than paying for college directly.

Without a good plan in place, this lingering debt obligation has the capacity to destroy any semblance of a comfortable retirement.

If you do find yourself in a situation where you are considering a private loan or parent PLUS loan, make sure you do your due diligence to understand all the common pitfalls.

Using Alternative Accounts for College Funding

While paying for college is a significant financial challenge, you don’t have to tie up all your resources exclusively for this purpose. There are alternative accounts that offer flexibility while addressing both college funding and retirement planning:

1. Cash Value Life Insurance: Cash value life insurance policies, such as whole life, offer a unique approach to saving for college and other financial goals. Here’s how they can be utilized:

-

- Access to Cash Value: You can withdraw or borrow against the cash value of the policy to cover college expenses or any other financial need. The advantage is that these withdrawals are typically tax-free up to the amount you’ve contributed (your basis).

- Tax Benefits: The growth of the cash value is tax-deferred, and when managed properly, you can access this money income tax-free in retirement.

- Flexibility: If your child doesn’t end up needing the funds for college, you still have a valuable life insurance policy that can provide financial security to your family.

- Estate Planning: Life insurance can also play a role in estate planning, providing a tax-efficient way to pass assets to your heirs.

- Misunderstandings: Life insurance is often misunderstood and maligned (sometimes for good reasons), but the right product with a trusted expert can provide a great long-term market buffer.

2. Roth IRA: While Roth IRAs are primarily designed for retirement savings, they have a unique feature that can be helpful for college funding:

-

- After-Tax Contributions: You do not take an income deduction on Roth IRA contributions, and therefore withdrawals are tax-free, provided you follow all the rules.

- Contributions: You can withdraw your contributions (cost basis) from a Roth IRA at any time without penalty or tax, making it a flexible option for college funding.

- Earnings: While it’s best to leave earnings in the account to maximize retirement growth, you can also withdraw them for qualified educational expenses without the 10% early withdrawal penalty (although you may owe income tax on the earnings).

- Retirement Priority: Keep in mind that prioritizing retirement savings in your Roth IRA is crucial, as these accounts are designed to provide income tax-free income during retirement.

3. Backdoor Roth: The Backdoor Roth IRA is an advanced strategy that allows high-income earners to circumvent the income limits associated with regular Roth IRA contributions. Here’s how it works:

-

- Contribution Conversion: You make a non-deductible contribution to a Traditional IRA up to the annual limit, regardless of your income.

- Conversion to Roth: After making the contribution, you convert the non-deductible IRA to a Roth IRA, essentially “backdooring” your money into a Roth account.

- Benefits for College and Retirement: The Backdoor Roth IRA allows you to contribute to a Roth IRA even if your income exceeds the limits. This can be a valuable tool for both college funding and retirement savings, as contributions can be withdrawn without penalty.

- A Word of Caution: Backdoor ROTH is an advanced strategy, and you should only do this in consultation with a financial advisor or a tax planner. Don’t attempt it on your own.

In all cases, the key to success is discipline. If you use these alternate accounts for college expenses, you should have a clear plan for replenishing and maximizing your retirement savings. While these options offer flexibility and tax advantages, you must carefully manage the trade-offs to ensure you’re meeting both your children’s educational needs and your retirement goals.

What Can You Do? Finding the Right Balance in College and Retirement Planning

Paying for your children’s education and securing your own retirement is a delicate balancing act. Here are some strategies to help navigate this financial dilemma:

- Plan Early: You will prevent massive issues in the future by saving as much as you can as early as possible. Feel like you got a late start? Start now! A well-thought-out financial plan can help allocate resources appropriately and make the miracle of compounding your friend!

- Set Adjustable Savings Goals and Automate Your Savings.

- Learn How to Reduce the Cost of College. Learn how the financial aid system works and the best way to access merit aid. Get off the rankings hamster wheel and cast a wide net in the college search. Find schools that want your student and will give money for them to attend. Learn all about financial aid appeals and merit aid leveraging.

- Consider All Options: Explore all options like traditional 529 plans, alternative strategies, scholarships, grants, and work-study opportunities. Encourage your children to take an active role in funding their education and have that conversation early. Consider affordable alternatives like community college or “lesser-tiered” in-state schools.

- Encourage Financial Literacy and Responsible Borrowing: If student loans are necessary, teach your children to make informed decisions and explore student loans with favorable terms. Make them financially responsible citizens at an early age!

- Consult a Financial Planner Who Understands the College Problem: We can help you bring efficiencies to your college and retirement planning with cashflow & tax strategies that keep you on the compounding curve while funding college.

Author:

Zaina Bankwalla

Further Reading:

My Kid Is a Decent Student but We Will Not Qualify for Need-Based Financial Aid